energy-tech

April 7, 2026

As Load Growth Accelerates, Utilities Tap Private Capital

Rising electricity demand in the U.S., driven by data centers, manufacturing and electrification of heating, is reshaping long-term planning and putting pressure on an already strained electricity grid. The North American Electricity Reliability Council has sounded the alarm in its reports on resource adequacy and the need for more generation resources and investments to meet future peak demand and maintain reliability. As a result of this load growth, utility investments into new and scaled-up generation assets are expected to rise along with grid infrastructure upgrades, mostly on tight timelines.

Utilities have traditionally financed capital expenditures through a combination of rate recovery and access to capital markets. Most utilities file rate cases with their state commissions or government to recover the investments in consumer bills. Utilities, investor-owned utilities (IOU) in particular, rely on issuing debt and equity to finance large, multi-year investment projects. However, a heightened scrutiny on consumer/member affordability, a rising cost of capital due to elevated interest rates and inflationary pressures are narrowing traditional pathways, at the same moment that capital needs are surging.

In the wake of these changes, private capital is playing an expanding role in the electricity sector. While private capital has long been a part of the electricity industry, both the scale and timing have shifted markedly over the last decade. Deloitte estimates that private investment comprises about 24% of total investments between 2017–2024, compared to 17% of total investments from 2008–2016. This change signals that private capital is moving from the margins toward a larger role in utilities’ investment strategies.

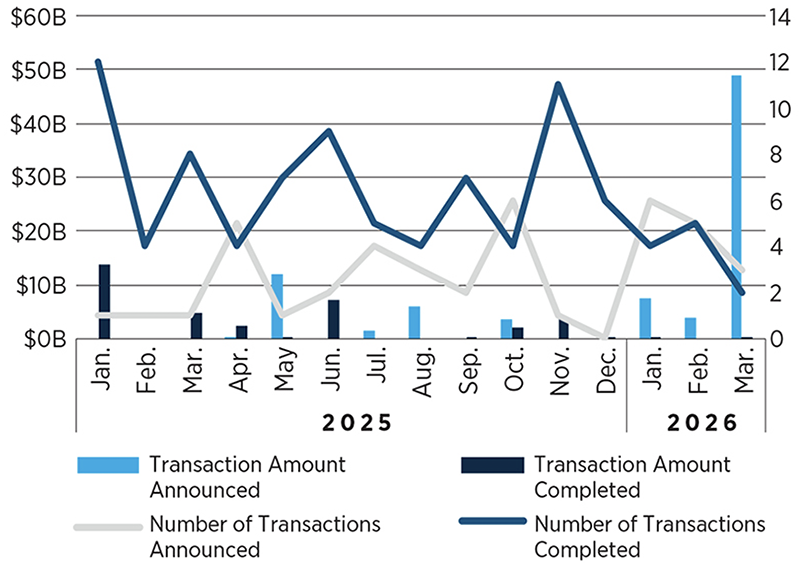

M&A Activity—Transaction Value & Volume

SOURCE: S&P Capital IQ.

From exploring various financing and equity deals to involving private financing earlier in the project cycle, investors and private capital seek opportunities for stable returns and offer the potential for lower rates. This trend is playing out on multiple fronts:

- First, utilities are freeing up capital and divesting through asset sales of non-regulated renewable assets like solar and wind plants.

- Second, regulated IOUs are seeking minority interest stakes or structured equity from private investors. This arrangement can provide some of the upfront funding for multi-year plans.

- Third, strategic partnerships like joint ventures can enable risk sharing and improve a utility’s credit profile.

- Finally, private capital firms are acquiring portfolios of assets or transitioning utilities to private ownership. Recent transactions underscore the scale of this shift. In March 2026, a BlackRock-led consortium agreed to buy AES Corporation for $33 billion, marking one of the largest privatizations in the power sector and highlighting growing investor appetite.

In the electric cooperative space, generation and transmission (G&T) cooperatives are also seeking to add new generation capacity to their portfolios. G&Ts are facing similar pressures and are turning to private capital to diversify their funding sources. There are three distinct ways in which G&Ts are adding generation resources, each with risks:

- First, through building and owning their own generation assets. While the most conventional route, cooperatives could face risks related to construction and the length of time to complete and operationalize the project.

- Second, G&Ts can acquire existing assets to add to their portfolio. However, this runs the risk of higher costs and capital expenditures associated with existing assets.

- Lastly, G&Ts are entering into joint ventures with private capital firms who build out the generation project. Depending on the structure of the venture, the risks could be higher if the two entities share the construction costs but lower if there is only a power purchase agreement (PPA). An example is Old Dominion Electric Cooperative announcing a long-term PPA with asset manager Blackstone. Blackstone will support the construction of the Wolf Summit Energy facility, a 600 MW combined-cycle natural gas power plant in West Virginia.

With S&P Global Research forecasting approximately $1.1 trillion in energy sector capital expenditures between 2025–2029, the question is no longer whether private capital will play a role but how it will shape asset ownership, risk allocation and system planning. As utilities and cooperatives respond to sustained load growth under economic and policy constraints, private capital is becoming an increasingly embedded feature of the financial tool kit.