economy

May 9, 2022

The American Dream: Sometimes It Just Doesn’t Add Up

“Don’t spend money on college. Work two jobs. Stop buying coffee. Start with a humble home.” This is the typical advice long-time homeowners tell those wanting to buy their first home today. It’s usually followed by, “I was 24 when I bought my first home for $80,000 because I worked hard and was frugal.”

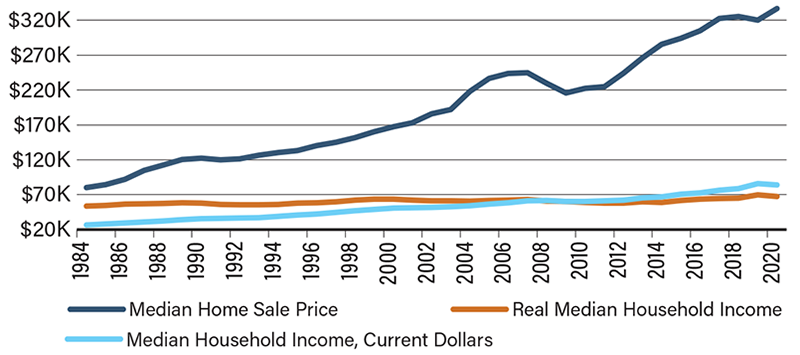

The median home price in 1985 was $84,275 while the median annual income was $26,433 ($54,334 in real terms), which means a typical home cost roughly 3.2 times nominal income (or 1.6 times real income). In 2020, the median home price and the median annual income were $336,950 and $84,003 ($67,521 in real terms), respectively. That means home prices were four times nominal income (or five times real income).

Those who take the advice to start with a humble home may also be out of luck as they face new competition from corporate investors. In 2021, 93 percent of homes purchased by corporations were well below the median price. These investors accounted for a record 18.4 percent of U.S. homes bought by the end of 2021.

Saving before buying a first home is also harder than it used to be as rent takes up a larger share of income today. The median monthly rent was $339 in 1985 and went up to $1,104 in 2020—a 225 percent increase. Real median income increased 24 percent over the same period. It doesn’t take Einstein to figure out that today’s renters have far less savings after essential expenses.

There is also no evidence suggesting that Americans don’t work as hard today since available data show that employees are working roughly the same number of hours. However, over half of would-be homebuyers today are contemplating working a second job, according to a survey by Bank of America.

Today, the American dream is far out of reach not because people aren’t working hard or budgeting well. Sometimes the math just doesn’t add up in their favor.

Median Home Price vs. Median Income (1984–2020)

Source: Federal Reserve Bank of St. Louis